Struggling with Stubborn Belly Fat That Just Won’t Go Away?

You’ve tried eating healthy. You’ve tried working out.

Yet those same problem areas remain… and it’s frustrating.

What if the real issue isn’t your diet…

but your body’s internal fat-burning switch?

FREE Training Video Reveals:

The Breakthrough Method to “Vaporize” Stubborn Fat Cells

(No extreme diets. No endless cardio. No stress.)

Discover how real people are finally burning fat, naturally and consistently.

Click below to watch your FREE training while it’s still online:

➡️ YES! Show Me The Free Video

Larry Humphreys, a retired Federal Emergency Management Agency worker in Moultrie, Georgia, said he and his wife’s monthly health insurance premiums have increased more than 40%, to $938, and they won’t be traveling much next year.

Humphries, 68, feels betrayed by the Federal Employees Health Benefits Plan. “As federal employees, we sacrifice high salaries in the private sector because we think government benefits will be better now when we retire,” he said.

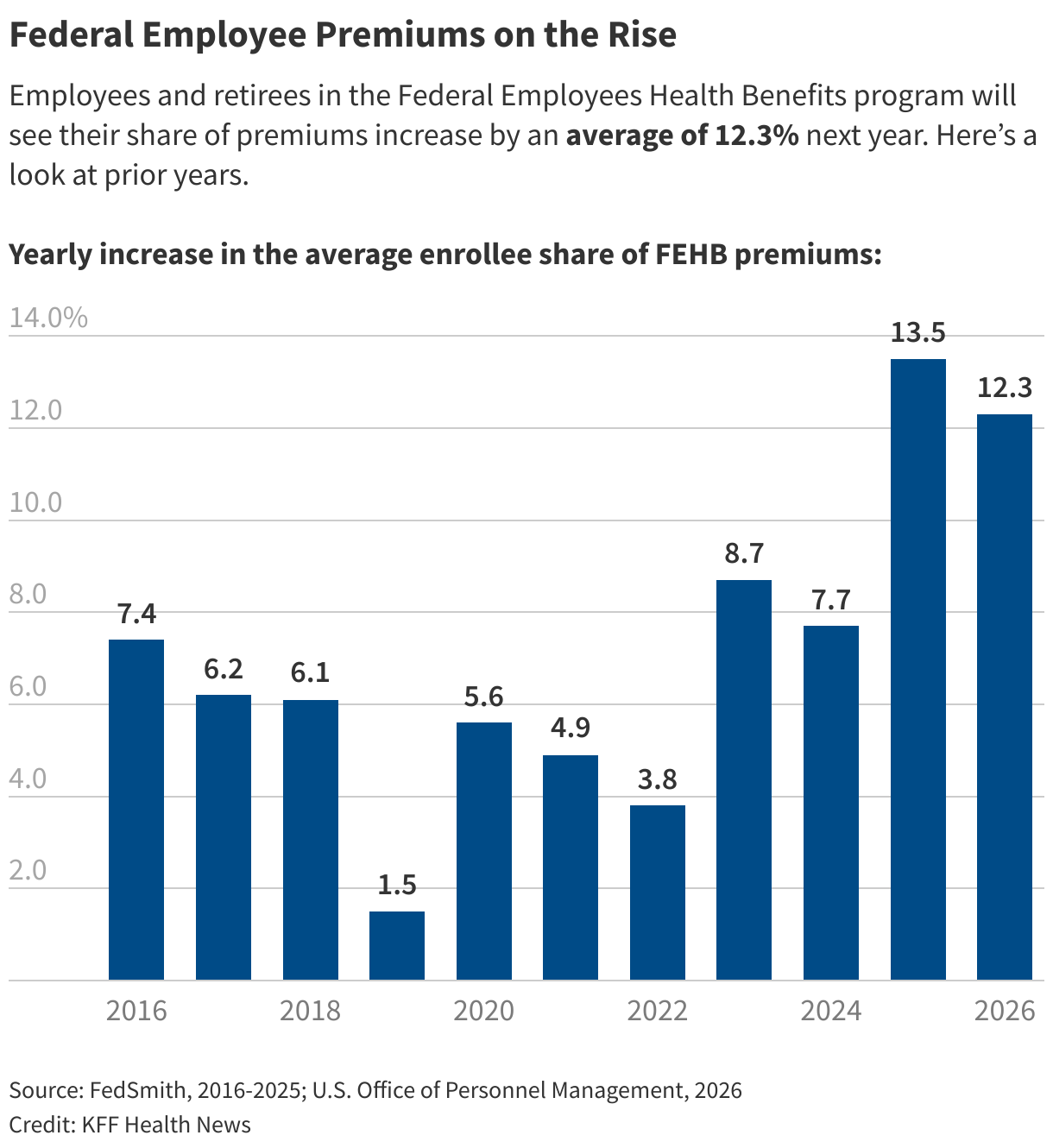

As the nation’s largest employer-sponsored health insurance plan, the FEHB plan covers more than 8.2 million federal government employees and retirees. The plan was once hailed as a national model for controlling costs while providing enrollees with multiple health plan options.

But next year, the system’s average insured premium will rise more than 12%, on top of a 13.5% increase in 2025. The increases in both years are higher than those experienced by many private employers and their workers.

FEHB’s rate hikes are similar to those for plans sold on Affordable Care Act exchanges — excluding the government subsidies that most enrollees receive, a major focus of debate on Capitol Hill. Premiums charged by insurance companies for Obamacare plans will rise an average of 26% by 2026, after rising 4% this year.

The latest FEHB premium increase is harder to swallow for millions of federal employees because of its timing: The 2026 increase was announced in October, when many federal workers were on unpaid leave during the 43-day government shutdown.

Unlike most private employers, FEHB plans offer their participants a variety of health plans to choose from. This allows some people to lower their monthly premiums by switching to a plan with a higher deductible or copay. But only about 5% of participants change plans each year, according to the Office of Personnel Management, which oversees the program.

Humphreys, who has stuck with the same health plan for decades despite steadily rising prices, said it’s difficult to determine which plan is best based on his health. He suffered from glaucoma and diabetes, and his wife, Julianne, also faced heart problems.

Their FEHB plan covers the cost of care not covered by Medicare, with Medicare typically paying 80% of the cost of care.

“There’s a concern that if you do something and you change your plans and it turns out to be wrong, you could get into trouble,” he said.

The open enrollment deadline for federal employees and retirees is December 8.

OPM said factors driving premium increases include an aging federal workforce, an increase in chronic disease and the use of prescription drugs, including the expensive GLP-1 weight-loss drug.

OPM said about 42% of federal employees are over the age of 50, compared with 33% of the general workforce. About 7% of federal employees are under 30 years old, compared with about 20% of workers overall.

OPM officials said the Trump administration’s policies aimed at lowering drug costs and focusing on preventing costly medical conditions are expected to help it control future premiums.

“Of course, none of these initiatives will happen overnight, and transforming a $79 billion ship will require slow and steady progress,” Shane Stevens, OPM associate director for health care and insurance, said in a release. “However, we are committed to improving our members’ quality of life and quality of care while ensuring that health care remains available and affordable for those who work (or have worked) for the American people.”

OPM did not respond to a request for comment.

John Holahan, a health policy researcher at the nonpartisan Urban Institute, said OPM’s explanation ignores a key reason for rising premiums: hospital consolidation. While FEHB plans are a collection of health plans, in many markets, including Washington, D.C., these insurers must negotiate with a handful of powerful health systems that have acquired other hospitals and physicians. That market power allowed them to drive up the price of the FEHB plan, he said.

“The costs patients incur depend not just on the care they receive, but also on how insurance companies choose to price, reimburse and limit access to that care,” Jacqueline D. Bowens, president and CEO of the Washington, D.C. Hospital Association, said in a statement.

Surprisingly, Holahan said, FEHB premiums are rising even faster than premiums for other small employers. But he’s not surprised that federal employees don’t change plans more often, even though it may be in their financial interests.

“People find the world of health care so complex,” he said. Holahan, a noted health economist, said he, too, found changing the Medicare health plan daunting.

Mike Lindquist, a scientific review officer at the National Institutes of Health, said he was unhappy with the increases in premiums over the past two years. “It’s difficult because it’s a big expense.”

Lindquist, 43, who lives in Brunswick, Maryland, has been participating in the same Blue Cross and Blue Shield plans through the FEHB program for the past several years, although he evaluates his options each fall.

“By not switching, you don’t have to worry about choosing a new program that might not take away your practitioners,” he said.

Jonathan Foley, a health consultant who served as a senior adviser to OPM during the Biden administration, said the premium increases will be a hardship for many enrollees. While FEHB plans offer a total of 200 health plans, with about 10 to 20 in each geographic market, enrollment is concentrated in a handful of Blue Cross and Blue Shield plans.

“This concentration reduces competition and has a dramatic impact on Blue Cross and Blue Shield’s price increases,” Foley said in an email.

The FEHB plan also faces higher costs because it requires its health plans to cover GLP-1 drugs such as Wegovy and Ozempic, he said. Nationwide, less than half of large employers offer the benefit, according to data from Peterson Health Care and KFF. KFF is a health information nonprofit organization that includes KFF Health News.

Another cost pressure since the start of the coronavirus pandemic is the increasing number of members taking advantage of behavioral health benefits to treat depression and anxiety, Foley said.

Foley said the Trump administration’s cuts to the federal workforce also contributed to increased costs. OPM lost about a third of its staff last year, he said, leaving fewer staff responsible for overseeing the FEHB plan and negotiating with dozens of health insurance companies.

“The Trump administration’s reduced workforce and unpredictability of policymaking have created considerable uncertainty for health insurance companies,” Foley said. “Actuaries responded to increased uncertainty by raising rates.”

A Government Accountability Office report this year found that recent OPM staffing vacancies led to the suspension of fraud risk assessments for the FEHB program.

John Hatton, executive vice president for policy and programs at the advocacy group National Association of Active and Retired Federal Employees, said rising prices mean it’s critical for FEHB members to shop and compare plans for next year. “The plan is to promote competition to mitigate and reduce costs,” he said.

Hatton said OPM surveys show the main reason people don’t change plans is that they’re overwhelmed by their options and worried about making a mistake. Switching to a plan with a slightly higher deductible can save you hundreds of dollars a month in premiums, he said.

But Humphreys, a Georgia retiree, said he likes the lower out-of-pocket costs the current plan provides for him and his wife. They owed very little money when his wife developed a kidney stone infection and sepsis and was hospitalized for 12 days.

That guarantee will soon come at a higher price: Next year, after taxes, their FEHB and Medicare premiums will account for more than half of his pension check.

“I could accept a plan with a lower premium, but that’s a gamble I’m not willing to take,” he said.

No title.